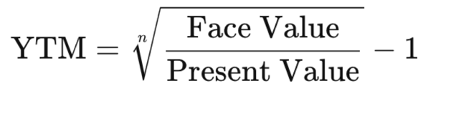

41 what is the duration of a zero coupon bond

Yield to Maturity (YTM): What It Is, Why It Matters, Formula - Investopedia May 31, 2022 · Yield to maturity (YTM) is the total return anticipated on a bond if the bond is held until it matures. Yield to maturity is considered a long-term bond yield , but is expressed as an annual rate ... Zero Coupon Bond | Investor.gov The maturity dates on zero coupon bonds are usually long-term—many don't mature for ten, fifteen, or more years. These long-term maturity dates allow an investor to plan for a long-range goal, such as paying for a child's college education. With the deep discount, an investor can put up a small amount of money that can grow over many years.

Solved QUESTION 1 What is the (Macaulay) duration of a - Chegg Finance questions and answers. QUESTION 1 What is the (Macaulay) duration of a zero-coupon bond with 4.3 years until maturity? QUESTION 2 Consider a bond with a (Macaulay) duration of 6.9 years. If the yield-to-maturity of the bonds falls from 3.0% to 2.0%, what will be the percentage change in the price of the bond?

What is the duration of a zero coupon bond

Bond duration - Wikipedia For a standard bond, the Macaulay duration will be between 0 and the maturity of the bond. It is equal to the maturity if and only if the bond is a zero-coupon bond. Modified duration, on the other hand, is a mathematical derivative (rate of change) of price and measures the percentage rate of change of price with respect to yield. Zero-Coupon Bonds: Characteristics and Examples - Wall Street Prep Generally, zero-coupon bonds have maturities of around 10+ years, which is why a substantial portion of the investor base has longer-term expected holding periods. PDF Understanding Duration - BlackRock rates, duration allows for the effective comparison of bonds with different maturities and coupon rates. For example, a 5-year zero coupon bond may be more sensitive to interest rate changes than a 7-year bond with a 6% coupon. By comparing the bonds' durations, you may be able to anticipate the degree of

What is the duration of a zero coupon bond. Understanding Bond Prices and Yields - Investopedia Jun 28, 2007 · A bond's coupon rate is the periodic distribution the holder receives. Although a bond's coupon rate is fixed, the price of a bond sold in secondary markets can fluctuate. For zero coupon bonds? Explained by FAQ Blog A zero-coupon bond doesn't pay periodic interest, but instead sells at a deep discount, paying its full face value at maturity. ... A coupon is a periodic interest received by a bondholder from the time of issuance of the bond till maturity. Zero coupon bonds, also known as discount bonds, do not pay any interest to the bondholders. Duration Definition and Its Use in Fixed Income Investing - Investopedia Sep 01, 2022 · Duration is a measure of the sensitivity of the price -- the value of principal -- of a fixed-income investment to a change in interest rates. Duration is expressed as a number of years. Bond ... Duration and Convexity to Measure Bond Risk - Investopedia Jun 22, 2022 · The duration of a zero-coupon bond equals time to maturity. Holding maturity constant, a bond's duration is lower when the coupon rate is higher, because of the impact of early higher coupon payments.

Zero Coupon Bond Value Calculator: Calculate Price, Yield to … Instead interest is accrued throughout the bond's term & the bond is sold at a discount to par face value. After a user enters the annual rate of interest, the duration of the bond & the face value of the bond, this calculator figures out the current price associated with a specified face value of a zero-coupon bond. Zero Coupon Bond Value - Formula (with Calculator) - finance formulas A 5 year zero coupon bond is issued with a face value of $100 and a rate of 6%. Looking at the formula, $100 would be F, 6% would be r, and t would be 5 years. After solving the equation, the original price or value would be $74.73. After 5 years, the bond could then be redeemed for the $100 face value. ZROZ PIMCO 25+ Year Zero Coupon US Treasury Index ETF Oct 20, 2022 · Learn everything about PIMCO 25+ Year Zero Coupon US Treasury Index ETF (ZROZ). Free ratings, analyses, holdings, benchmarks, quotes, and news. What is the duration of a zero coupon bond? - Quora What is the duration of a zero coupon bond? - Quora Answer (1 of 12): Everyone is telling you that duration is a weighted average of time until you get the cash flows. That is a bad way to think about duration. It is a measure of risk. The Macaulay Duration of a zero is the time to maturity. The Modified Duration is a better measure.

Duration Definition and Its Use in Fixed Income Investing - Investopedia The duration of a zero-coupon bond equals its time to maturity since it pays no coupon. What Are Types of Duration Strategies? In the financial press, you may have heard investors and... What Is a Zero-Coupon Bond? Definition, Characteristics & Example Typically, the following formula is used to calculate the sale price of a zero-coupon bond based on its face value and maturity date. Zero-Coupon Bond Price Formula Sale Price = FV / (1... The One-Minute Guide to Zero Coupon Bonds | FINRA.org After 20 years, the issuer of the bond pays you $10,000. For this reason, zero-coupon bonds are often purchased to meet a future expense such as college costs or an anticipated expenditure in retirement. Federal agencies, municipalities, financial institutions and corporations issue zero-coupon bonds. Zero-coupon bond - Wikipedia A zero coupon bond (also discount bond or deep discount bond) is a bond in which the face value is repaid at the time of maturity. Unlike regular bonds, ... A zero coupon bond always has a duration equal to its maturity, and a coupon bond always has a lower duration. Strip bonds are normally available from investment dealers maturing at terms ...

What is the duration of a zero-coupon bond that has eight ...

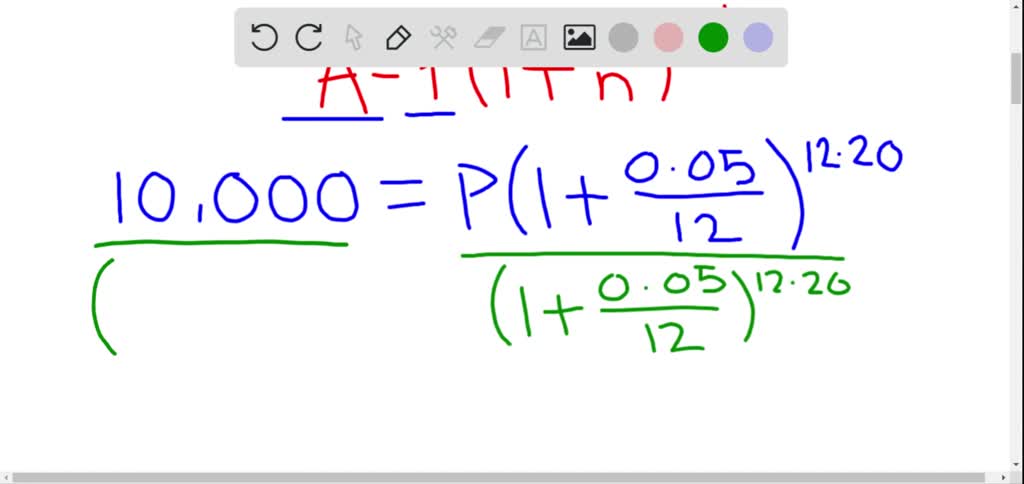

The Macaulay Duration of a Zero-Coupon Bond in Excel - Investopedia Calculating the Macauley Duration in Excel Assume you hold a two-year zero-coupon bond with a par value of $10,000, a yield of 5%, and you want to calculate the duration in Excel. In...

Zero-Coupon Bond - Definition, How It Works, Formula | Wall ...

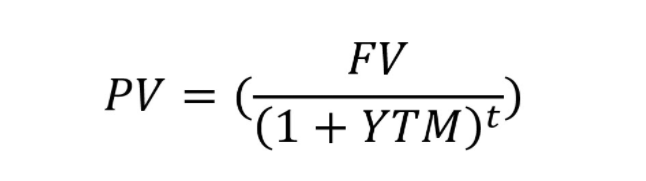

Zero Coupon Bond - (Definition, Formula, Examples, Calculations) Thus, the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19. The difference between the current price of the bond, i.e., $463.19, and its Face Value, i.e., $1000, is the amount of compound interest that will be earned over the 10-year life of the Bond.

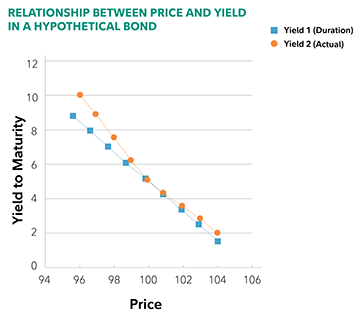

Aha! Interest rates do matter.

United States Treasury security - Wikipedia Treasury bonds (T-bonds, also called a long bond) have the longest maturity at twenty or thirty years. They have a coupon payment every six months like T-notes.. The U.S. federal government suspended issuing 30-year Treasury bonds for four years from February 18, 2002, to February 9, 2006. As the U.S. government used budget surpluses to pay down federal debt in the late …

Zero-coupon bond price as a function of time to maturity for ...

Zero-Coupon Bond - Definition, How It Works, Formula John is looking to purchase a zero-coupon bond with a face value of $1,000 and 5 years to maturity. The interest rate on the bond is 5% compounded annually. What price will John pay for the bond today? Price of bond = $1,000 / (1+0.05) 5 = $783.53 The price that John will pay for the bond today is $783.53. Example 2: Semi-annual Compounding

Price of a defaultable zero coupon bond price in each time t ...

Zero-coupon bond - Wikipedia A zero coupon bond (also discount bond or deep discount bond) is a bond in which the face value is repaid at the time of maturity. Unlike regular bonds, ... A zero coupon bond always has a duration equal to its maturity, and a coupon bond always has a lower duration. Strip bonds are normally available from investment dealers maturing at terms ...

Zero Coupon Bond Price Calculator Excel (5 Suitable Examples)

Advantages and Risks of Zero Coupon Treasury Bonds - Investopedia The responsiveness of bond prices to interest rate changes increases with the term to maturity and decreases with interest payments. Thus, the most responsive bond has a long time to maturity...

a zero coupon bond is a bond that is sold now at a discount and will pay its face value at the tim 7

Zero Coupon Bond Calculator – What is the Market Price? - DQYDJ P: The par or face value of the zero coupon bond; r: The interest rate of the bond; t: The time to maturity of the bond; Zero Coupon Bond Pricing Example. Let's walk through an example zero coupon bond pricing calculation for the default inputs in the tool. Face value: $1000; Interest Rate: 10%; Time to Maturity: 10 Years, 0 Months ...

Zero Coupon Bonds

Should I Invest in Zero Coupon Bonds? | The Motley Fool So for instance, a 10-year zero coupon bond priced when prevailing yields were 3% would typically get auctioned for roughly $750 per $1,000 in face value. The $250 difference would...

A 12.75-year maturity zero-coupon bond selling at a yield to ...

What Is a Zero-Coupon Bond? - Investopedia The maturity dates on zero-coupon bonds are usually long-term, with initial maturities of at least 10 years. These long-term maturity dates let investors plan for long-range goals, such as saving...

Impossible Finance — The Perpetual Zero Coupon Bond | by ...

Zero Coupon Bond Calculator - What is the Market Price? - DQYDJ Duration of a bond is a length of time representing how sensitive a bond is to changes in interest rates. Since zero coupon bonds have an equal duration and maturity, interest rate changes have more effect on zero coupon bonds than regular bonds maturity at the same time. (Whether that's good or bad is up to you!)

Duration: Understanding the Relationship Between Bond Prices ...

Zero Coupon Bond Value Calculator: Calculate Price, Yield to Maturity ... Instead interest is accrued throughout the bond's term & the bond is sold at a discount to par face value. After a user enters the annual rate of interest, the duration of the bond & the face value of the bond, this calculator figures out the current price associated with a specified face value of a zero-coupon bond.

Key Rate Duration | Financial Exam Help 123

PDF Understanding Duration - BlackRock rates, duration allows for the effective comparison of bonds with different maturities and coupon rates. For example, a 5-year zero coupon bond may be more sensitive to interest rate changes than a 7-year bond with a 6% coupon. By comparing the bonds' durations, you may be able to anticipate the degree of

Advanced Bond Concepts: Duration | The Financial Engineer

Zero-Coupon Bonds: Characteristics and Examples - Wall Street Prep Generally, zero-coupon bonds have maturities of around 10+ years, which is why a substantial portion of the investor base has longer-term expected holding periods.

Zero Coupon Bonds Explained (With Examples) - Fervent ...

Bond duration - Wikipedia For a standard bond, the Macaulay duration will be between 0 and the maturity of the bond. It is equal to the maturity if and only if the bond is a zero-coupon bond. Modified duration, on the other hand, is a mathematical derivative (rate of change) of price and measures the percentage rate of change of price with respect to yield.

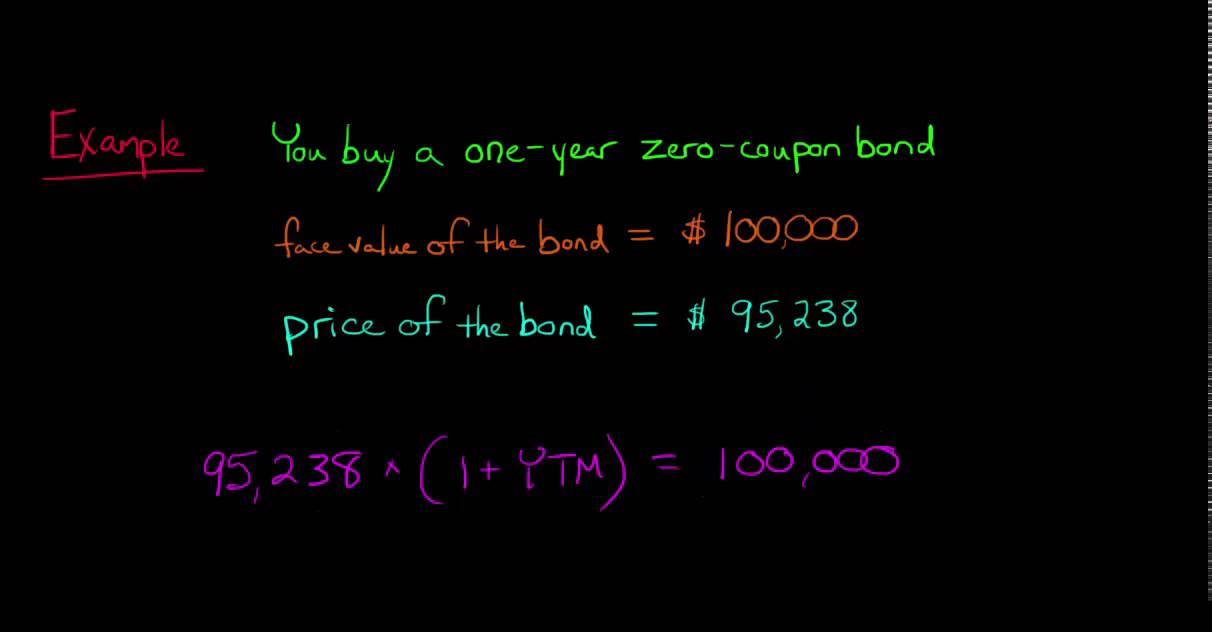

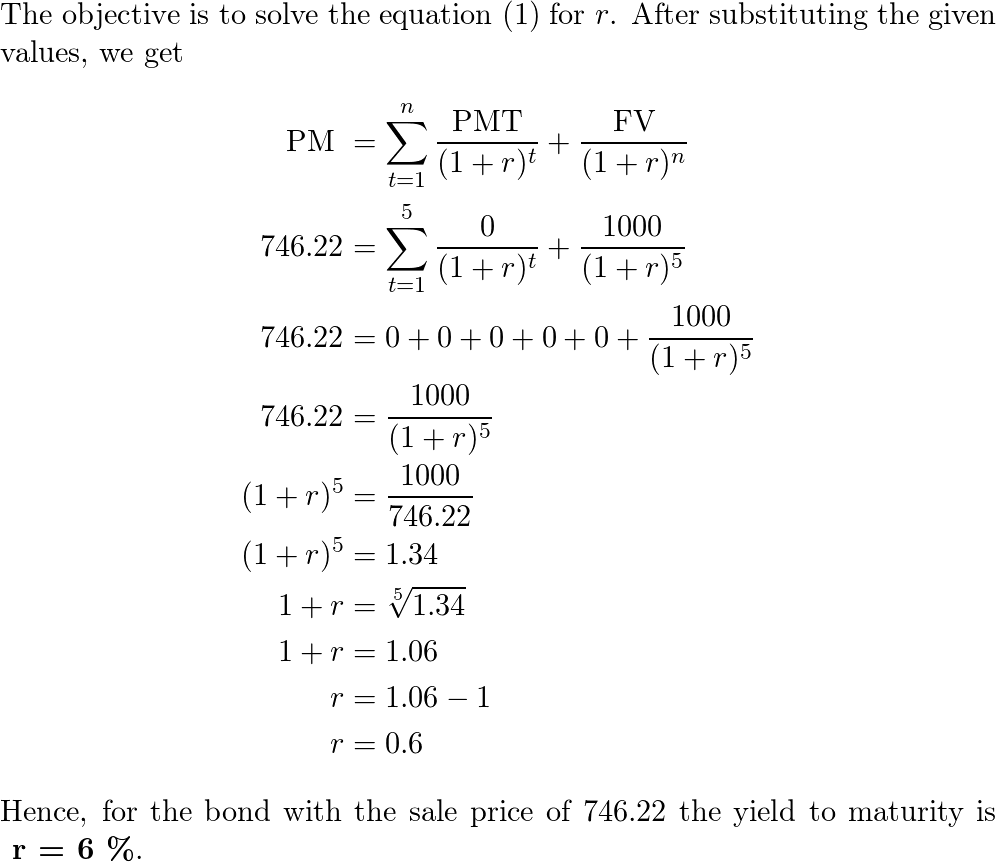

Calculating the Yield of a Zero Coupon Bond

MGT338 - Chapter 6: Valuing Bonds | Team Study

Zero-Coupon Bond - Definition, How It Works, Formula | Wall ...

PDF) Introduction to Duration | Adnan Zafar - Academia.edu

Zero Coupon Bond Value - Formula (with Calculator)

What is a Zero Coupon Bond? Who Should Invest? | Scripbox

THE DURATION OF A BOND AS A PRICE ELASTICITY AND A FULCRUM

Zero Coupon Bond Vs Regular Coupon Bond - Fintelligents

Solved a. What is the duration of a zero-coupon bond that ...

Zero-Coupon Bond - Definition, How It Works, Formula | Wall ...

Zero Coupon Bonds Explained (With Examples) - Fervent ...

Zero Coupon Bond -Features, benefits, drawbacks, taxability ...

A zero-coupon bond with face value $1,000 and maturity of fi ...

What Is Duration of a Bond? - TheStreet Definition - TheStreet

hullwhite - Hull-White zero-coupon bond price does not depend ...

Valuing a zero-coupon bond | Mastering Python for Finance ...

Invest in Zero Coupon Bond at Yubi | Learn All About It

Solved] You are managing a portfolio of $3.0 million. Your ...

![PDF] Duration and convexity of zero-coupon convertible bonds ...](https://d3i71xaburhd42.cloudfront.net/39b5487ce4f8becdfb0faf5ae6e30fd10537436c/13-Figure5-1.png)

PDF] Duration and convexity of zero-coupon convertible bonds ...

Problems 63–66 involve zero-coupon bonds. A zero-coupon bond is a bond that is sold now at a discount and will pay its face value at the time when it matures; no interest payments are made. ...

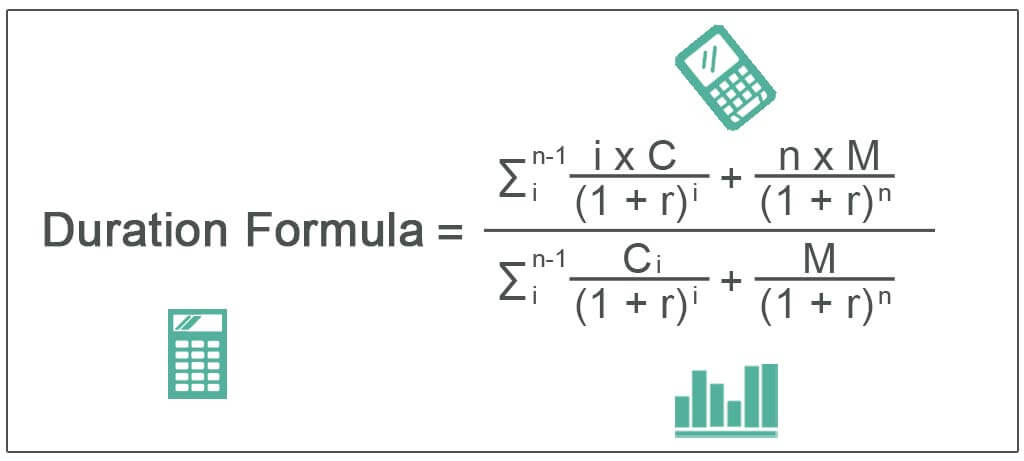

Duration Formula (Excel Examples) | Calculate Duration of Bond

Yields & Prices: Continued - ppt video online download

Modified duration of zero-coupond bond (FRM practice question)

Solved] ou find a zero coupon bond with a par value of ...

Modified Duration - Zero Coupon Bond Modified Duration ...

Finding YTM of a Zero Coupon Bond (6.2.1)

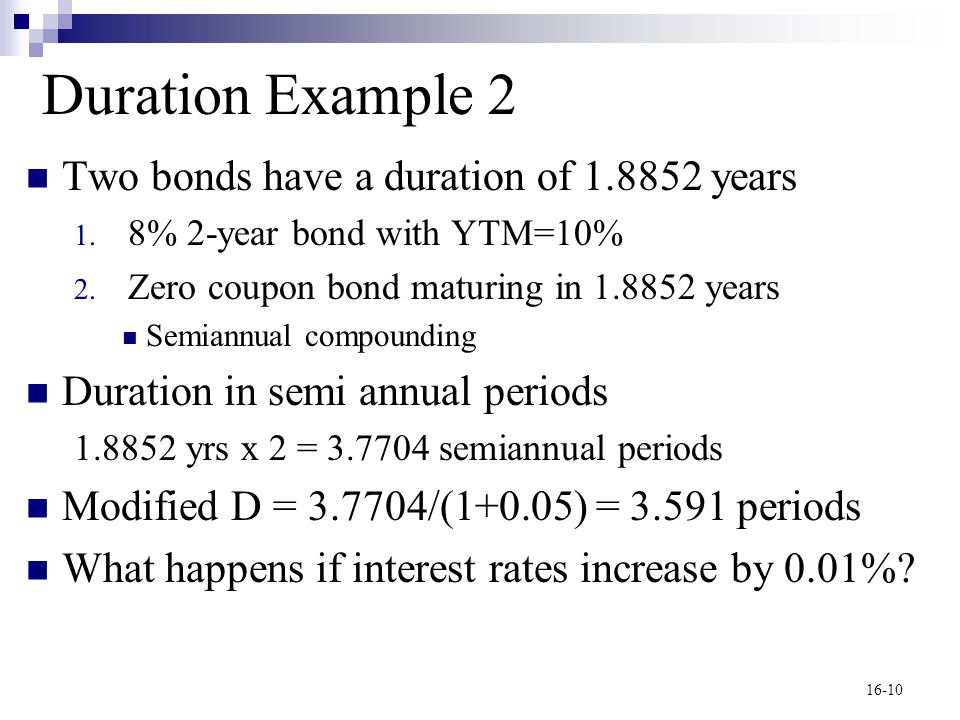

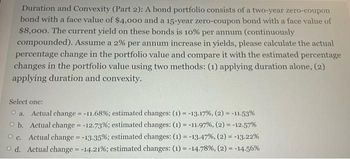

Answered: Duration and Convexity (Part 2): A bond… | bartleby

Post a Comment for "41 what is the duration of a zero coupon bond"